In its May 2012 Statement on Monetary Policy, the RBA included this graph on the price declines of individual commodities.

The analysis of recent developments is less gloomy, although the year-on-year declines are considerable.

What happens to prices will largely depend on Chinese demand and the

prognosis on that is generally not a confident one by most

commentators.

What happens to prices will largely depend on Chinese demand and the

prognosis on that is generally not a confident one by most

commentators.

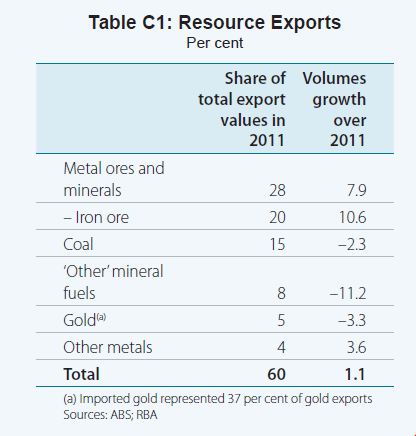

The RBA discusses Australia's resource exports. In relation to iron ore, the depth of Australia's dependence on China is revealed:

The analysis of recent developments is less gloomy, although the year-on-year declines are considerable.

The [commodity price] index remains at a historically high level, but is around 9 per cent lower than its peak in mid 2011. In general, commodity prices have been supported by the gradual pick-up in global economic activity since the start of the year, though increases in some prices have been partially retraced over April. Spot prices for iron ore and base metals have all increased, while spot prices for both thermal and coking coal have declined in recent months, largely reflecting increased supply. Australia’s terms of trade are estimated to have declined further in the March quarter, as average export prices for bulk commodities continue to decline gradually from their September 2011 peak.

The RBA discusses Australia's resource exports. In relation to iron ore, the depth of Australia's dependence on China is revealed:

Iron ore is Australia’s most significant export, accounting for around 20 per cent of total export values in 2011. The primary destination of Australia’s iron ore exports is China, which accounted for around 70 per cent of iron ore export volumes in 2011, while Japan and Korea imported most of the remaining 30 per cent. Iron ore volumes grew by 10½ per cent over 2011, which is slightly slower than the average annual pace of growth over the past decade. In early 2011, iron ore export volume fell owing to production disruptions from a higher than average number of cyclones in the north of Western Australia. However, iron ore export volumes recovered strongly over the rest of the year to reach new highs, reflecting expansions in the capacity of mines and rail as well as some improvements in the utilisation of port facilities.