Introduction

One of the major markers of globalisation since the 1970s has been the incredible expansion of the financial sector - a phenomenon known as financialisation. The financial sector expanded in virtually every country in the world. Since this time the process of financialisation (defined as the expansion of both domestic and global finance) has been been in retreat as has financial globalisation (defined by cross-border financial flows only).

The global crisis, not surprisingly, has been primarily responsible and it will take quite some time for capital flows to recover, especially if the European financial crisis deepens. The expansion of credit/debt has stalled and the excesses of pre-crisis finance continue to be worked out of the system, Over the medium-term, even in the absence of another systemic financial crisis, it is likely that financialisation will be restricted by global deleveraging as excessive indebtedness is worked out of the world economy.

Nevertheless, wariness about financial instability will continue to be challenged by financial innovation and the possibilities for profits in new financial products. Despite arguments that the global financial crisis showed the need for better regulation of financial markets, it is not clear that this view has overcome the arguments of financial interests for few substantial changes to regulation. Financialisation continues to progress in developing countries and financial globalisation will recover as the world economy recovers.

The issue for the future is whether a financialised world political economy is inherently prone to a cycle of crisis, retreat, recovery, stability, excesses, crisis. While it is possible to argue that financialisation has reached a high point in many developed economies, it is likely that developing countries will become even more important global financial players in coming years - both as recipients and investors.

In Australia, the financial sector has grown rapidly since financial liberalisation in the 1980s. The cyclical downturn in the financial sector has not been as extreme and Australian banks are in rude health compared to banks in other developed economies. The solid performance of the Australian financial system has been helped by the government's willingness to support the financial system during the crisis and the avoidance of recession. The household sector remains highly indebted and foreign debt remains at highest ever levels. Any renewed expansion of credit will increase Australia's medium-term financial vulnerability. Policy-makers should be aiming to foster a period of consolidation in the Australian financial markets and the property sector.

Financialisation and Financial Globalisation

According to

McKinsey, global financial assets increased from about US$12 trillion in 1980 to US$206 trillion in 2007.

Financial depth (defined as financial assets as a percentage of GDP) increased from 120 per cent to 355 per cent over the same period. By 2012, financial assets had increased to $225 trillion, but compared to world GDP they had declined by 43 per cent (54 per cent if government debt is excluded). Declines have occurred in both developed and developing countries. Developing countries are significantly less financialised than developed countries with financial depth of 157 per cent compared to 408 per cent. China's financial depth (226 per cent) is considerably lower than that of the United States (463 per cent - down 37 per cent from 2007 up to mid 2012), Japan (453 per cent) and Western Europe (369 per cent) , with India (148 per cent) lower still.

Finance progressively detached itself from the 'real' economy with just over a quarter of the rise in financial depth between 1995 and 2007 related to households and non-financial corporations. This is astounding given the extensive growth of mortgage markets in virtually all developed economies.

These figure above relate to the growth of finance generally, but if we consider cross-border movements of capital (an integral component of globalisation alongside trade) it is clear that the process has gone backwards since the crisis, declining substantially since 2007 from $11.8 trillion to around $4.6 trillion in 2012.

Most of the fall (70 percent) is accounted for by Western Europe - a substantial reversal of financial integration as European banks have retreated from cross-border lending. Central banks have become more important in cross border flows in Europe, accounting for over 50 percent of capital flows. Cross-border flows have fallen from 20 per cent of global GDP in 2007 to 6 per cent in 2012, a remarkable decline.

Capital flows involving developing countries have rallied since the debacle of 2008-09. Developing countries have increased their share of cross-border flows from 5 per cent in 2000 to 32 per cent in 2012. More capital flowed out of developing countries than flowed in - US$1.8 trillion compared to US$1.5 trillion.

Financial globalisation (i.e. cross-border financialisation) is still extensive with around 30 per cent of global equities and bonds owned by foreigners (54 percent for Europe, 23 per cent for North America and 9.4 per cent for China).

Australia

Australia, of course, has been a willing participant in the process of financialisation. A recent

speech by Malcolm Edey, Assistant Governor (Financial System) at the Reserve Bank of Australia, reveals the extent of the financialisation of the Australian economy up to 2007 and its retreat after the crisis.

Edey points out that credit to GDP "increased from around 50 per cent in the mid 1980s to around 160 per cent in 2007". Total banking system assets "rose from around 50 to around 200 per cent of GDP" and "foreign exchange turnover increased by a factor of more than 30 in nominal dollar terms over that quarter-century, when the nominal economy itself expanded only by a factor of 4½.

The process of financial liberalisation began in Australia in the late 1970s and accelerated through the mid-1980s. Although many people seem to have forgotten Australia had a serious financial crisis in the late 1980s to early 1990s, which ironically may have helped us in the global financial crisis as banks remained more cautious through the 1990s and early 2000s.

The graph below shows just how much Australian financial sector assets have increased over the past 25 years.

The Australian banking sector avoided the excesses of some banking systems such as Ireland, Iceland, the United Kingdom and France among others. US problems lay outside of an extensive build up in banking assets.

The wealth management sector has also expanded since the 1980s, although much of that has to do with a new 'regulation' of enforcing superannuation payments for all Australians in work - hardly de-regulation. As Edey points out:

Funds under management (principally in superannuation and life offices) expanded from around 30 to around 130 per cent of GDP between 1985 and 2007, broadly matching the growth rate seen in the deposit and loan sector. And, of course, there has been a huge growth in services related to asset and risk management, including securities and derivatives trading.

Both managed funds and securitisation took a big hit from the financial crisis, but all sectors have been affected, reversing the process of financialisation. Continuing woes in Europe are likely to see many investors less amenable to risk. Although this can change rapidly as investors often seem to have short memories. The recent rise of the share market would be worrying many of those who sold out of equities and encouraging many to get back in, which will further inflate the share market, possibly setting it up for a large correction down the line.

Another impact of liberalisation has been the decline in interest rate margins. This is despite the fact that the Australian banking sector is dominated by the big 4 banks. While it is easy to point to the costs of liberalisation in terms of the tendency towards crisis, it is important to remember that easier access to credit has benefits as well.

As Edey points out the post-liberalisation financial system

changed profoundly in other ways than just size. One was in its degree of openness to competition and in the nature of that competition. The post-Campbell reforms allowed market forces to work, and opened up the system to new competitors. ... Deregulation ended the artificial rationing of bank loans, making credit much more widely available ... the cost of financial intermediation came down very substantially. ...

The rationing that existed in the old regulated environment had encouraged banks

to compete on a ‘whole of institution’ basis, rather than at the level of

individual product lines. ... In this situation, wide interest margins were used to cross-subsidise

payment services, and customer mobility was limited because loyalty to a bank

was one of the critical factors in obtaining access to scarce loans.

Deregulation changed that model by allowing innovators to compete separately for

the most profitable lines of business. Cross-subsidies in the banking system

were competed down, and this helped to drive the reduction in net interest

margins.

If given a choice between going back to the old system of regulated banks and credit or staying with the current system with all its problems, most would choose the latter, especially if it were explained that it would mean less access to credit. But this is obviously part of the problem too, greater willingness to extend credit during periods of asset price ebullience can lead to deteriorating lending standards increasing the possibilities of

non-performing loans down the line. Thus far this has not occurred in Australia, with the excellent growth performance of the Australian economy providing a sound macroeconomic environment (low unemployment) and a cautious household sector increasing saving.

Banks have also remained extremely profitable, which has been reflected in their share prices.

Still

household indebtedness remains close to pre-crisis highs, which makes households and the wider economy vulnerable to changing macroeconomic conditions and a decline in international financial supply. Housing-related debt accounts for 81.6 per cent of household interest payments to income and 90 per cent of debt to income. Interest payments as a percentage of disposable income have come down from their pre-crisis peak, but are still higher than they were in the late 1980s when mortgage rates reached 17 per cent! (see

Table B21)

Competition in the banking sector until recently was mainly on the lending side of the equation, but as banks have sought alternative sources of funding, competition for deposits has increased. Banks have reduced their reliance on short-term debt and securitisation has also declined from a lower base.

The wholesale funding mix for banks has also shifted away slightly from overseas sources, but clearly the major change is away from short-term funding.

The high level of debt build-up from the 1990s to 2007 has stabilised in the post-crisis years. Australians have returned to saving. The share market has recovered and

property continues to tread water.

Not surprisingly, credit growth in all sectors has been flat in recent years.

A renewed property boom runs the risk of reversing this trend, leading to a bigger adjustment down the track. Having built up their debt share so high households can only increase their leverage at the cost of higher vulnerability. This is one of the reasons the RBA needs to take care when regulating new lending products and lowering interest rates further, without compensating policies from the government to discourage housing speculation.

Australian households are now more connected to the financial sector, through higher levels of debt and forced saving through Australia's superannuation system. The Australian economy is also more connected to the global financial system. Banks and other corporates have increasingly turned to offshore sources for funding.

Currently, according to the RBA's Deputy Governor

Guy Debelle, "domestic markets have benefited from strong international demand for Australian

dollar assets. Local issuers continue to be viewed favourably by offshore

investors looking to diversify credit exposures."

Extensive foreign liabilities mean that Australia will continue to remain vulnerable to changes in international financial sentiment, although it needs to be noted that Australia has recently passed a very severe test during the GFC. Many other countries have not been so lucky with stagnant growth and continuing financial trials.

Financialisation affects us all and it is policy that must determine the balance between the individual benefits of increased access to credit and the possibilities of financial instability. Australia's financial sector remains sound but an eventual recession will test the financial sector and its growth in Australia, especially if lending standards deteriorate over the next few years.

Conclusion

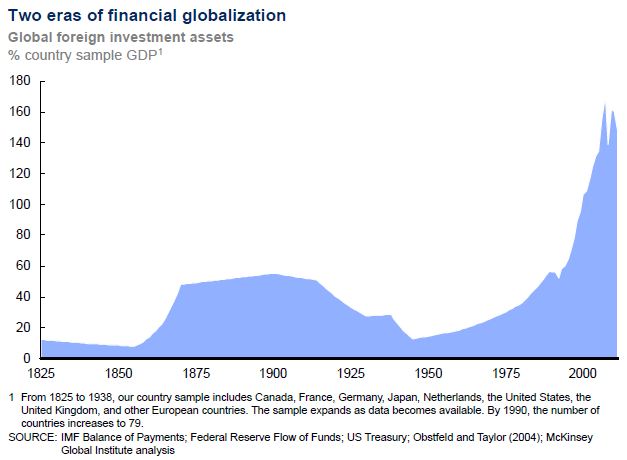

Financial globalisation has ebbed and flowed over the past couple of hundred years. The period before World War One is often called the golden age of capitalism but it ended in war and economic depression. It took a long time for financial flows to recover, but recover they did.

Despite some setbacks in recent years, the world economy remains highly globalised and financialised. In considering whether the current period is a permanent reversal or just a pause in the two distinct but related processes, requires detailed analysis of political processes in the major economies of the world. It seems unlikely that United States policy-makers will change their mind on the benefits of financial liberalisation and financialisation, but a prolonged period of economic stagnation could have an impact on this predilection.

Virtually the entire world adheres to a form of capitalism and while not all policy-makers in all countries are equally sanguine about globalisation, very few currently believe that the solution to development requires a full scale retreat into isolation.

This could change, however, if globalisation is blamed for growing inequality and political chaos. It may be the turn of developed countries to support alternatives to globalisation if economic crisis continues to affect growth and the distribution of wealth and income across societies. Democratic polities cannot necessarily be blamed for looking to more insular alternatives if increasing globalisation is associated with rising inequality and instability.